More Thoughts on Planet

I sold some Planet Labs (PL) stock today as I took a deeper look into some of the companies’ financial filings. I am still long, but I am more cautious going forward. Let’s look at a couple factors giving me some pause.

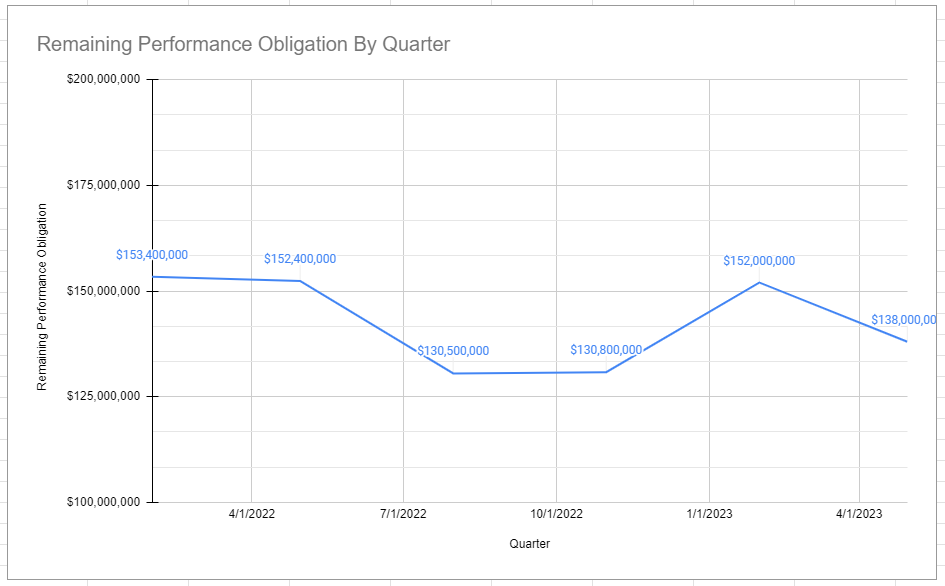

Remaining Performance Obligation

PL defines Remaining Performance Obligation as follows:

Remaining performance obligations represent the amount of contracted future revenue that has not yet been recognized, which includes both deferred revenue and non-cancelable contracted revenue that will be invoiced and recognized in revenue in future periods.

The key word is “contracted.” This amount represents signed contracts and illustrates some degree of customer commitment to PL. In other words, if a customer is willing to sign a contract with PL and commit to paying the company for its mapping services, then the RPO over time should show the degree of customer commitment. Further, given PL focuses on the number of customers at the end of period (EoP) as a sign of interest in their services, it is reasonable to expect that more customers would lead to higher RPO. But the data tell a different story:

Over the last 18 months or so, the RPO has fluctuated between $130 - $150 million. Meanwhile the number of customers has increased from “over 700” to “over 900.” So, what gives?1

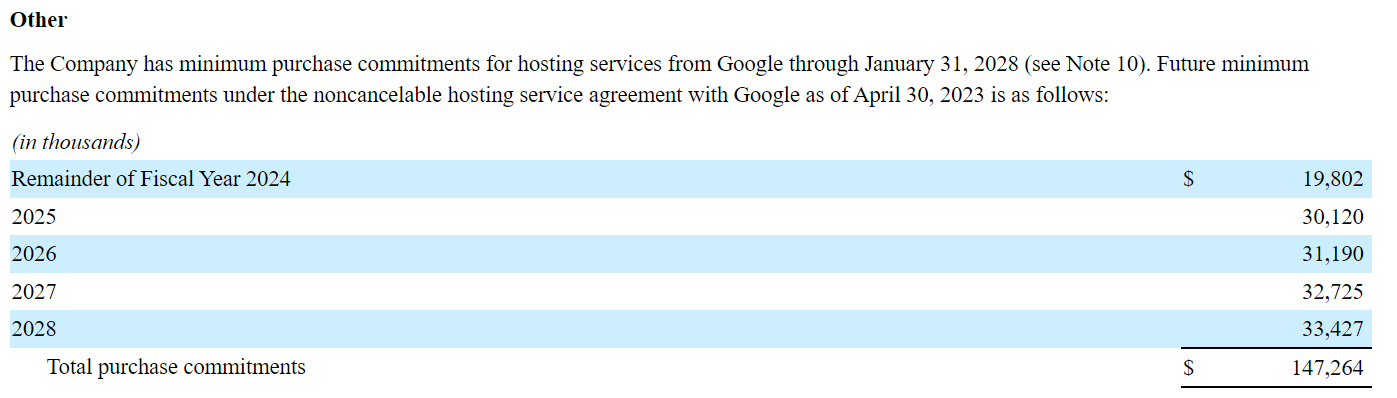

Related Parties - Google

A well known bull factoid is that Google owns about 11% of PL.2 This 11% represents 31.9 million shares, valued at about $105 million. What is lessor known, maybe, it that PL is committed to buy cloud hosting services from Google over the coming years. From the latest 10-Q:

In other words, PL is committed to pay Google about $150 million through 2028 for cloud hosting services. This represents a not so insignificant amount of PL’s operating expenses going directly to a related party. It’s troubling because one could imagine PL being able to shop this contract to Microsoft or AWS to lower hosting costs and improve operating leverage. But it doesn’t seem like they can given their purchase commitments to Google. This is particularly troubling because Google is offering a basic off the shelf service in a highly competitive market place, and yet PL chooses to stay with them. It just raises more questions in my mind.

I am long PL.

I know, EOCL has a termination for convenience clause so it is not included in RPO. But still, the number should be trending up with more customers, no?

Though with dilution that number is going lower by the day.

References:

Planet Labs - 10Q (July 24, 2023)

Planet Labs (PL) (June 18, 2023)

Planet (PL) V (April 1, 2023)

Planet Earnings (September 17, 2022)

Planet Labs (June 15, 2022)

Planet Labs II (April 16, 2022)

Planet Labs (December 21, 2021)