Planet Labs

Planet Labs (PL), recently came public via Special Purpose Acquisition Corporation (SPAC). The company describes itself as follows:

Planet Labs PBC provides daily satellite data and insights about earth. The company designs, builds, and operates earth observation fleet of imaging satellites, capturing, and compiling data. It serves agriculture, civil government, defense and intelligence, drought response, education and research, energy and infrastructure, finance and insurance, forestry and land use, mapping, maritime, sustainability, and federal sectors. Planet Labs PBC was formerly known as Planet Labs Inc. Planet Labs PBC was founded in 2010 and is based in San Francisco, California.

In the registration statement the company, describes its strategic advantages:

We deliver a differentiated data set: a new image of the entire Earth landmass every day. To collect this powerful data set, we design, build and operate hundreds of satellites, making our fleet the largest Earth observation fleet of satellites in history. Our daily stream of proprietary data and machine learning analytics, delivered through our cloud-native platform, helps companies, governments and civil society use satellite imagery to discover insights as change happens.

To help further our mission, we have developed advanced satellite technology that increases the cost performance of each satellite. This has enabled us to launch large fleets of satellites at lower cost and in turn record over 1,700 images on average for every point on Earth’s landmass, a non-replicable historical archive for analytics, machine learning, and insights. We have advanced data processing capabilities that enable us to produce “AI-ready” data sets. As this data set continues to grow, we believe its value to our customers will further increase.1

Planet’s business strategy was further expounded in their investor presentation on November 18, 2021.2 Will Marshall, Planet’s founder and CEO, noted the following:

Let me just kick it off, a little bit about the vision. I think there’s three key messages that are most important about Planet and for you all to take away. One is that Planet is a data subscription business. We sell beta feeds. We don’t sell satellites. We sell beta feeds into people’s workflows that enables those entities to make smarter decisions. Fundamentally, we’re a data subscription business and that means high margins and high growth. You’ll see that in our financials.

Secondly, Planet has data that is relevant to a wide variety of vertical markets, so we have a massive market opportunity. We’ll describe some of that.

Finally, we have a significant lead. Planet really welcomes the competition. I think it’s great. It is also true, in our area, especially the data as a daily scan, no one else has anything like it and that’s what services a huge set of markets and we’ll talk that through.

So from a strategic and business case perspective, Planet focuses on three perceived strengths: (1) the company provides a high margin, subscription business, (2) Planet supports a number of vertical markets, and (3) Planet has a significant lead versus the competition.

Another thing that stuck to me is that Planet is vertically integrated:

We pioneer that with a vertical map, complete vertical integration from the design of the satellites to the operation of the satellites, to the imagery analytics that sit on top of that. That vertical integration enables us to take the latest ask from a customer and iterate that.

Further, the company stated that their satellite imagery is often integrated into their customer’s systems, so a customer will have a hard time switching to a competitor if they are reliant on the info from Planet. The company talks about layering features into its imagery, or “stacks”, to add additional information to customers. In the agricultural vertical market, the company described it in this way:

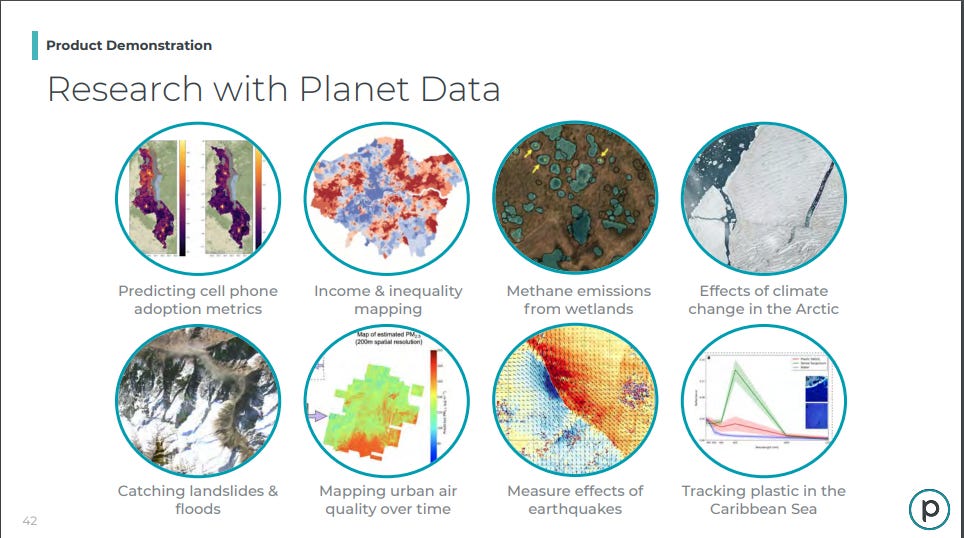

These companies use our data to scan large areas of land to help farmers improve their crop yield. Our data enables the improvement of crop yield because we have a spectral band called near infrared that enables us to tell biomass or even pull-out crop type and crop yield in every 3- by 3-meter box of every farmer’s field around the world every day. That enables the farmer to determine when to add water, when to add fertilizer, when to harvest, steps that enable more efficient crop production. We’ve seen increases of 20% to 40% of increase in crop yield and similar reductions in fertilizer use. Product improvements go up significantly by agricultural companies that use our data. Ours is the only data set that covers that wide variety, 25% of the landmass of the Earth is agriculture, so you just can’t do that with a tasked system that has existed before Planet.

Summary

In sum, Planet has highlighted the following advantages of its business and value proposition to customers:

Data subscription business-Planet compares itself to Bloomberg:

“It’s a bit like Bloomberg Terminal but for Earth data. We have a terminal, so this is financial services industry with data feeds that you can bespoke set up, so it’s very similar. Just like Bloomberg Terminal, high growth, high margins, and high stickiness. It’s very hard, once you get these into your workflows, there’s high switching costs.”

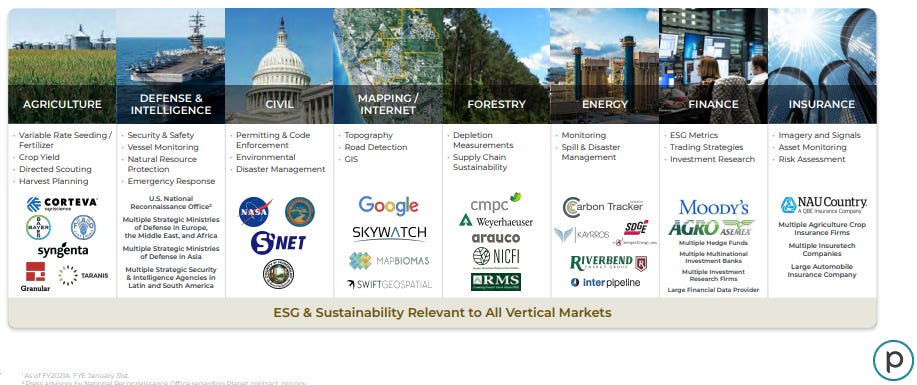

Planet serves multiple vertical markets.

Planet has a lead over its competitors.

The company provides information to its customers that adds value and improves output.

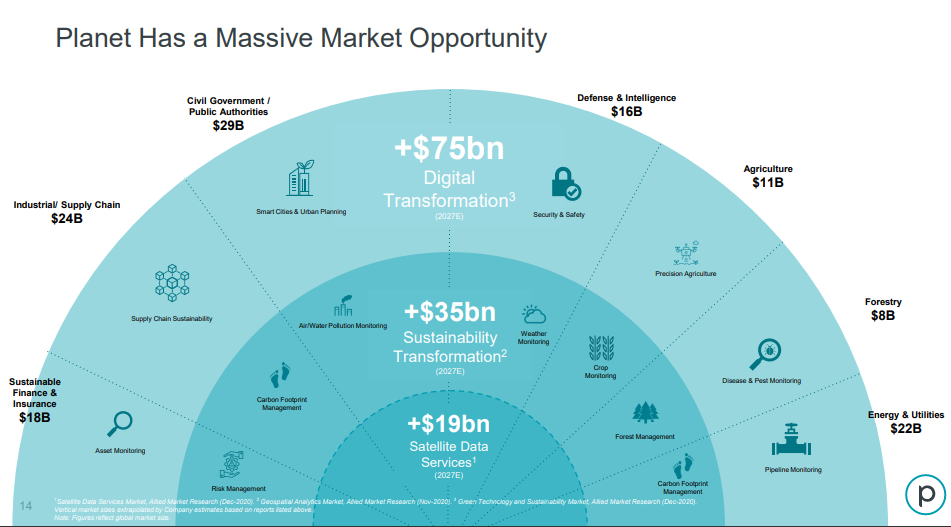

Total Addressable Market

Looking at Planet’s investor presentations, the company included a slide that highlights the markets it supports:

The company claims that the total addressable market for its services is $128 billion:

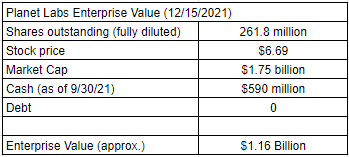

Enterprise Value

I calculated Planet’s EV as follows:

Note: This is a bit of an estimate/guess because I could not find up to date information on the cash balance and debt. Planet reported receiving $590 million as part their merger with DMYQ.

Planet is not profitable. The company projects FY 2022 revenue (ending January 2022) at $130 million. The company projects 2026 revenue to be $693 million.

Investor

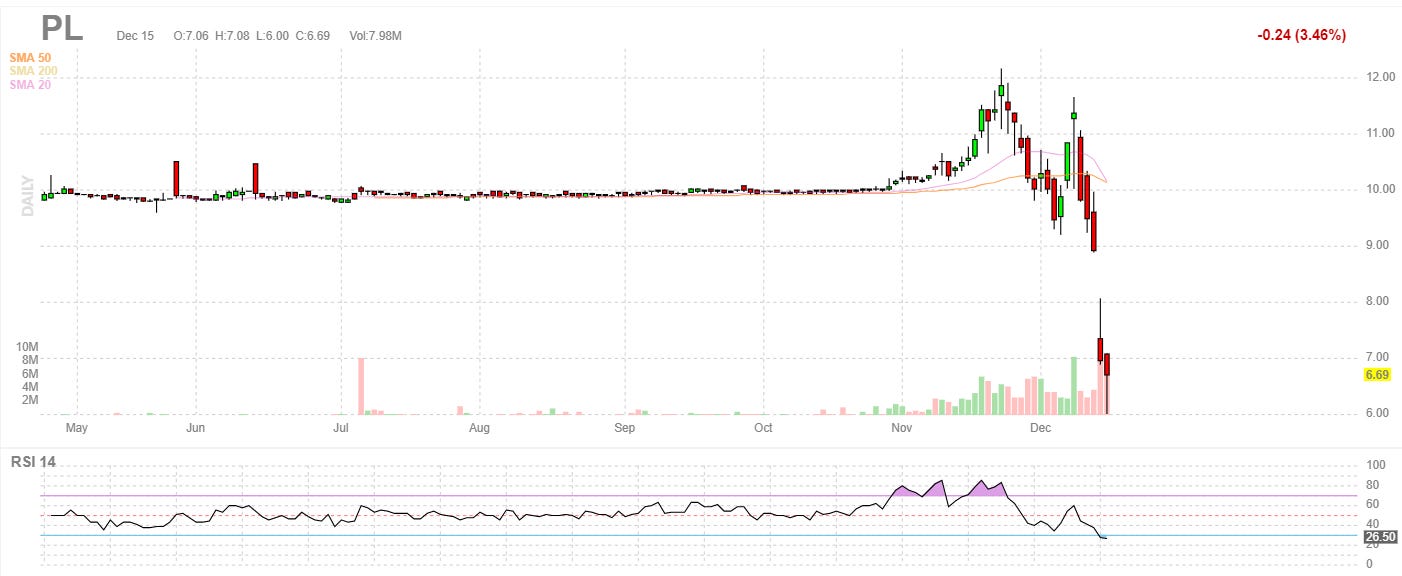

Of note, Planet has strong investor backing, including Google and Marc Benioff. Google owns over 10 percent of the company. However, the stock chart is not inspiring:

Concluding Thoughts

I like Planet Labs. But, it is hard to make a case that it is a good investment based on the financials. Though, there is a case to be made that if Planet is able to leverage its operating strengths, it may be able to generate significant cash flows down the line. If the $128 billion TAM figure is close to accurate, there is a lot of potential with this company. Further, there is a case to be made that Planet could be a good strategic fit for an existing software business, as an add on service to an existing platform. Time will tell. For the moment, I would stay on the sidelines with Planet.

https://d18rn0p25nwr6d.cloudfront.net/CIK-0001836833/000baa7f-7133-4555-94c3-8b564f074543.pdf (pg. 244)

https://www.sec.gov/Archives/edgar/data/1836833/000119312521336589/d242006d425.htm