Planet Earnings

Planet Labs (PL) released earnings on September 12th, for their 2nd quarter (fiscal year) 2022. Overall, I thought the numbers were pretty good and the company is making some progress increasing their customer base, growing revenues, and demonstrating (to some degree) the uptake of their services.

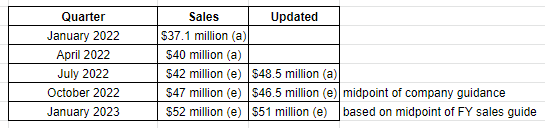

Looking at revenues, PL reported sales of $48.5 million for the quarter. That is a 20% increase in sequential quarter sales. The chart below is an updated version of a previous analysis I did from the last quarter. The idea is to try to predict sales for the next couple quarters based on the companies’ own projections.

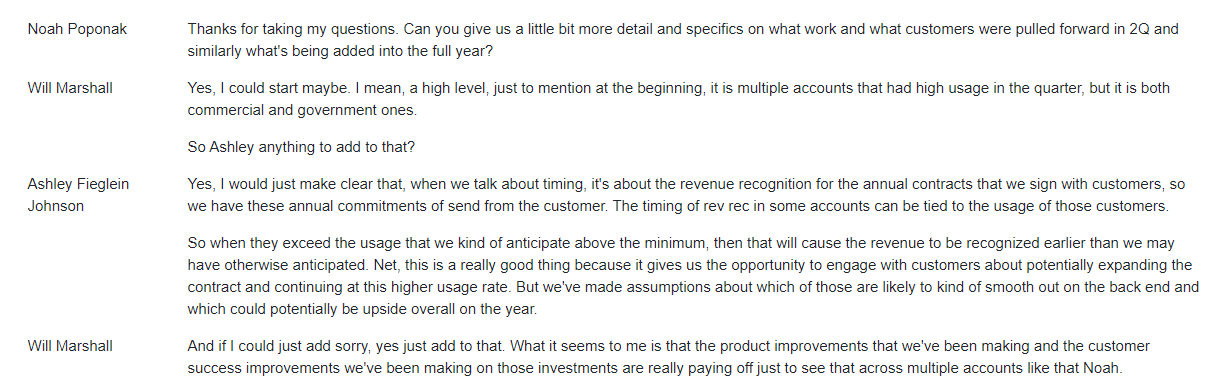

Of note, PL reported much higher revenue for the 2nd quarter than the companies own guidance. (Planet projected revenue for the quarter between $41-$43 million) This is how PL management explained the strong sales growth in Q2:

It is interesting that PL customers appear to have higher usage of their contracts than the company expected, which translated into increased sales. And the company appears to have made some assumptions about how the usage will “smooth out” in the next couple quarters. That will be interesting to see in the next earnings release. If their customers are increasing usage of PL’s services and run up against contract limits, will they increase the contract amount or slow their usage? I think that will be the big signal in the Q3 earnings release.

A couple other points stuck out to me:

PL is not really getting any closer to profitability. It looks like they will be increasing spending in order to invest in future growth opportunities.

PL is supporting three customer verticals: agriculture, defense and intelligence, and civil government. And there are a number of interesting anecdotes about customers improving their cattle grazing based on their use of PL mapping services or climate disaster response with civil governments. But it is hard to get a sense of how much traction they are having in expanding into new verticals (e.g. insurance or finance). That is another signal I will be looking at in the next quarter. Another challenge is that PL does not disclose revenue by vertical so it is hard to get a sense of which vertical is driving growth.

Management noted their ability to respond to customer needs related to map latency. This is a good example of where PL’s products might provide a durable competitive advantage. If customers are demanding more real time mapping and PL is able to invest in the technologies to support that need it would show some degree of nimbleness is being able to meet customer wants in a competitive sector. To me that would make the product more “sticky”.

Remaining Performance Obligations (RPO) was down quarter over quarter. This is a comparison of RPO between this quarter and the last:

On the surface, this appears to be a negative. But, PL management noted that RPO does not include government contracts, such as ECOL, that contain termination for convenience clauses. According to PL management, the backlog amount is more than double RPO.

Conclusion

PL seems to be on the right track. But the stock is not really that attractive at current prices. PL has an enterprise value of about $1.3 billion and sales will be about $186 million for 2023. And I still do not have a good sense of where growth is going to come from. PL does seem to be doing a good job of penetrating existing, established verticals and there is probably some future growth opportunities there, but I have not seen anything that suggests the company is any closer to making inroads in new verticals. I have a small position in PL and I might look to add if the stock falls a little bit, but I want to see more color on where the company is headed before I would consider buying more aggressively.

I am long PL.

Prior Posts in Planet Labs:

Plant Labs, Mixed Quarter - Q1 FY 2023, June 15, 2022

Planet Labs II, Taking a Closer Look, April 16, 2022

Planet Labs, Mapping the World, December 15, 2021