Planet Labs II

I previously wrote about Planet Labs (PL) in December 2021. This is a company that is serving a growing market for satellite data and intelligence in multiple sectors. PL came public via a SPAC and has been among a list of high profile de-SPACs that have fallen hard in the midst of a market downturn, higher interest rates, and growing inflation concerns.

PL is growing a myriad of sales and utilization metrics at a nice clip, but the company is not profitable. And looking under the hood a bit, the company is not really close to any type of sustainable profitability. This is a company that will likely burn through capital for a few years in the hopes of growing its customer base and demand for its services. In sum, there is not much of a margin of safety with PL.

The inherent challenge I face trying to analyze PL is my lack of competence in the subject matter. I do not have the technical knowledge to understand what differentiates PL from its competitors and what customers are looking for in its product offerings. This is further compounded by the fact that I am relying heavily on what the company itself is reporting to investors. This is information it controls and will more likely paint a cleaner picture. The company has a strategy of what the future will look like and they want investors and other stakeholders to buy into their strategy. This will undoubtedly bias the way they tell their story. To mitigate some of this concern, I endeavor to focus more on financial signals, like cash flow and sales growth that would confirm whether their strategy is bearing fruit.

Public Benefit

One aspect that I had not explored previously is that PL is a public benefit corporation, not a traditional C corporation. This is how the company describes its public benefit status:

Public Benefit: Our business model is aligned with our mission and public benefit purpose: to accelerate humanity toward a more sustainable, secure and prosperous world by illuminating environmental and social change. We are dedicated to the continuous pursuit of creating an unbiased, scientifically accurate, and trusted source of data about the changing planet.

Source: PL 2021 10-K

This is a novel designation and time will tell how this impacts PL’s growth. However, the public designation status is listed as a risk factor for the company as well. Specifically, PL noted:

The company may not achieve its public benefit purpose.

The public benefit nature of PL may be at odds with maximizing shareholder value as PL may take actions that may not benefit shareholders if it serves the public benefit.

The company is less likely to be a takeover target because the acquirer would need the same public benefit provisions in their charter unless 2/3s of PL shareholders vote for the acquisition. This seems unlikely as management has concentrated voting power via class B shares.

My takeaway is that the public benefit corporation designation for PL is a slight negative for shareholders, but I don’t really know. It is a bit speculative to imagine a situation where PL management seeks to benefit the public interest over shareholders. But the takeover provisions related to being a public benefit company is probably a negative for PL. If it is harder for a potential suitor to buy the company, that removes some optionality from PL shares.

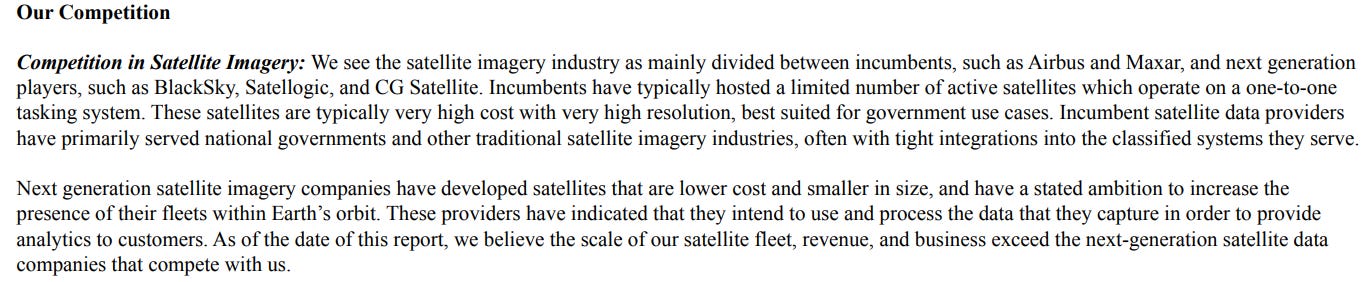

Competition

PL operates in a pretty competitive market. In their latest 10-K, PL explained that investment in space over the past 10 years has decreased the satellite launch costs and has opened up satellite data services beyond the defense industry. This has opened up the market for a number of satellite data providers, including Maxar, PL, and BlackSky. PL notes a number of sectors such as forestry, supply chain, and energy, that would now have access to satellite data to inform decision making. This is how PL describes it competitive position in the satellite industry:

In the next generation space, PL appears to be the bigger player compared to BlackSky. In its Q4 2021 earnings report, Blacksky reported that the company is projected to grow 2022 revenues to between $52-$56 million, with 14 operating satellites. Meanwhile PL has about 200 operating satelites and is expected to grow revenue to between $170-$190 million.

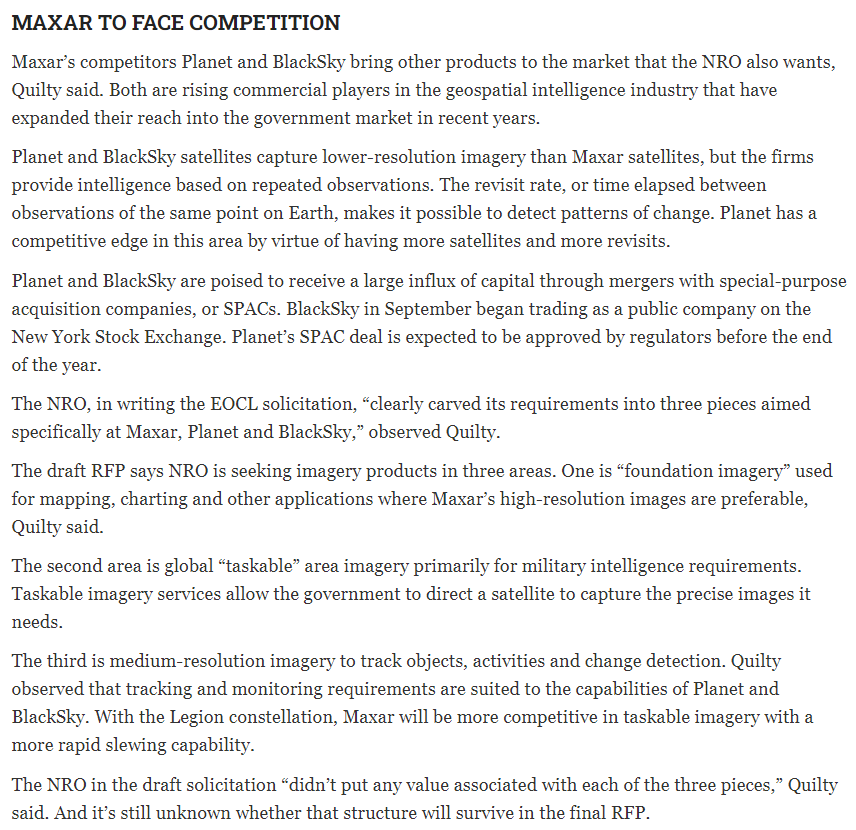

In the near term, these companies are awaiting an announcement from the National Reconnaissance Office (NRO) on the awarding of the EOCL contract. This award is expected to benefit Maxar, PL, and BlackSky. Though, it will likely depend on utilization. A recent Space News article provided good coverage of the competitive landscape:

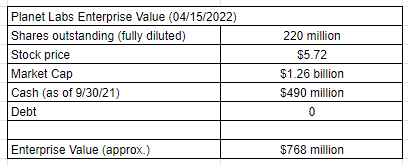

Enterprise Value (EV)

I calculated PL’s current EV as follows1:

In my previous post on PL, I estimated the EV as about $1.16 billion. But, looking back, I clearly overestimated the share count as at least 40 million or so shares are earn out shares and warrants that are out of the money. PL’s share price would need to rise into the $10-20 range for these shares to become truly outstanding. As of January 2022, PL had a book value of about $650 million, most of which is made up of cash, property, plant, equipment, and goodwill. (See page 78 of the 2022 10-K) In sum, PL trades about 2X book value.

Stock Chart

Below is the stock chart for PL. Since the de-SPAC, the general trend has been lower. Though, the stock appears to have found some support in the low $5 price range. Technical analysis, or any attempt to use past price and volume action to predict the future price is a highly imperfect exercise. One could easily look at this chart and see both and uptrend (in the shorter term time frame) and downtrend (more long term trend). My best guess is that the chart seems to show some accumulation and support in the $5 price range.

Earnings Trend

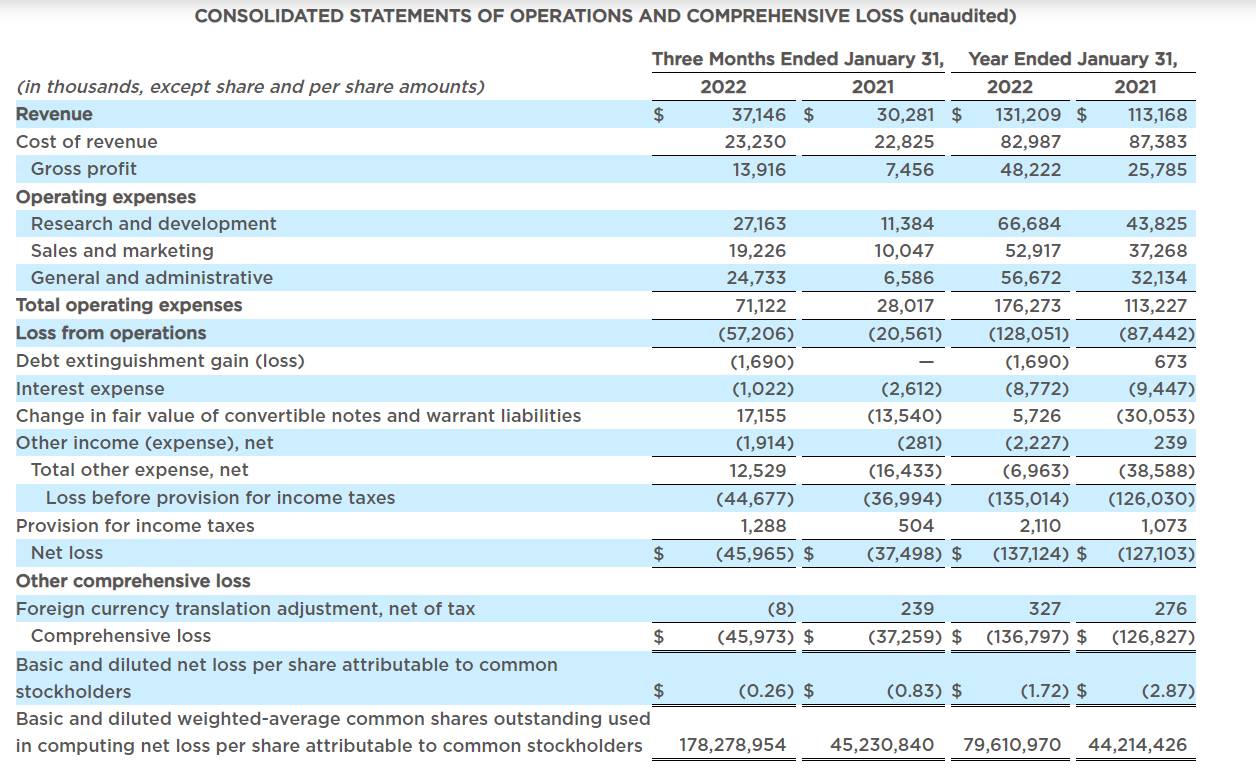

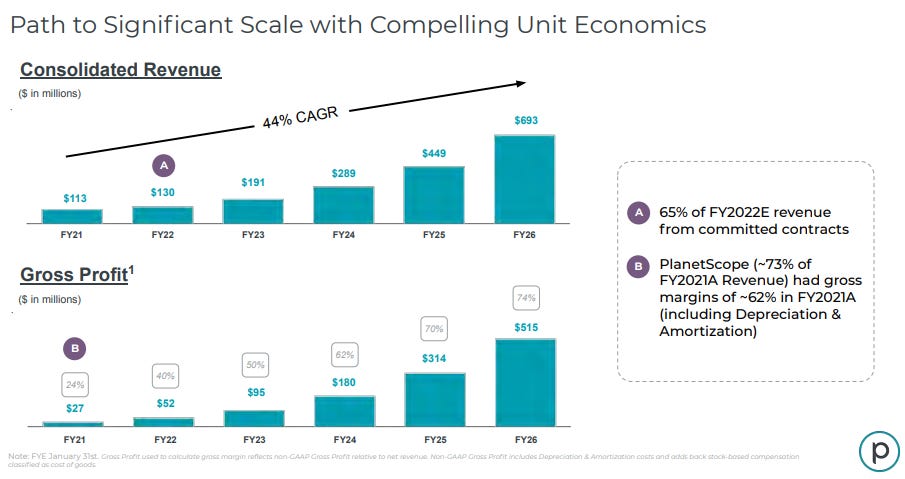

On March 31, 2022, PL reported earnings for its full year 2022 and provided guidance for its 2023 fiscal year ending January 2023. For the year ended January 2022, PL reported sales of $131 million and projects sales of between $170-$190 million for the year ended January 2023. The company also reported increasing its customer count by 25% to 770 for the year and announced a number of partnerships and initiatives. Gross margins are expected to be in the 40-50% range. This is the income statement from the press release:

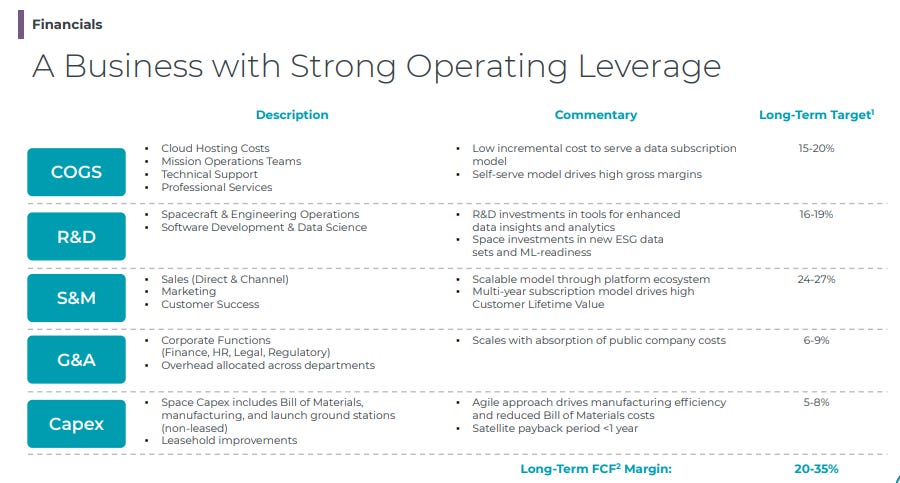

While gross margins are pretty good on the surface, the operating expenses really stuck out to me. PL is hemorrhaging cash, spending $2 for every $1 they bring in. Though operating cash flow for 2022 (-$42 million) paint a little better picture, the company is still on track for negative cash flow for the time being. It was really striking to me what little operating leverage there is for PL. There were a couple slides from a September 2021 Analyst day presentation that provide some context to this:

The bull case for PL is that the company will be able to grow revenues and improve scale, but that is still an open question. For example, for 2022, PL reported revenues of $131 million (on target), but gross profit of about $48 million (below the $52 million target). It will be important to keep track of how PL is able to scale this business in the future.

Conclusion

To date, PL seems to be executing pretty well. The company has hit revenue targets for 2022 and projects 2023 revenues at $170-$190 million for 2023. This is below their September 2021 Analyst day projections for 2023 of $191 million in sales. But the company could be playing the earnings expectations game so I would not read too much into the 2023 sales forecasts. I like PL, and I do own stock in the company.

But at this valuation there does not seem to be any margin of safety. I wonder how big the satellite imagery market really is. I have no doubt there is a growing niche of sectors that would benefit from PL’s data, but is it really as big as PL and other companies claim it is? I am not sure. The bull case for PL is that there is large, unmet need for satellite data and ancillary information like water levels or temperatures their stacks might be able to provide. The bear case is that the market is really not that big and companies would not pay for a standalone satellite imagery service or even as part of a stack/API. Meanwhile, satellite imagery is competitive and, at least for now, pretty capital intensive. And I also wonder about how PL’s data or mapping is really any better than a competitors’. A map is a map, no? Is speed such a big deal? Time will tell.

I do have a position in PL.

The EV calculation is based on my best estimates of the current share count. This was a challenge for me. I started with the shares outstanding (about 260 million class A &B shares outstanding as of April 11, 2022 (see the second page of the 2022 10-K), and subtracted the earn out shares and warrants that are out of the money. This is obviously a best estimate on my part.