Planet Labs (PL)

Bob Seger had a song, Against the Wind, that I heard on the radio the other day and it got me thinking a little about Planet Labs (PL). It is instructive to read how PL describes itself:

Planet is a leading provider of global, daily satellite imagery and geospatial solutions. Planet is driven by a mission to image the world every day, and make change visible, accessible and actionable. Founded in 2010 by three NASA scientists, Planet designs, builds, and operates the largest Earth observation fleet of imaging satellites. Planet provides mission-critical data, advanced insights, and software solutions to over 880 customers, comprising the world’s leading agriculture, forestry, intelligence, education and finance companies and government agencies, enabling users to simply and effectively derive unique value from satellite imagery.

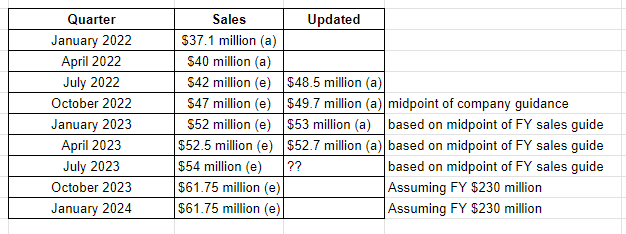

At a current stock price of $3.36, PL has an enterprise value of about $550 million, which includes about $375 million in net cash (no debt). PL is not profitable and recently lowered FY 2024 sales estimates from $248-$268 million to between $225-$235 million. So taking the midpoint, that’s $258 million to $230 million, or 11% less than three months ago. This is my quick and dirty analysis of quarterly sales:

So even while PL reduced FY 2024 sales estimates by 11%, the company is still projecting robust sales growth over the rest of the year ending January 2024. It is an open question whether they’ll still be able to hit these projections. The market seems doubtful.

[DISCLAIMER: I am not an expert on this company or sector. So do not rely on this information or analysis as a basis for investment. This is a highly speculative piece that is for information purposes only. At the time of this writing, I do have a position in Planet Labs. But that could change at a later date.]

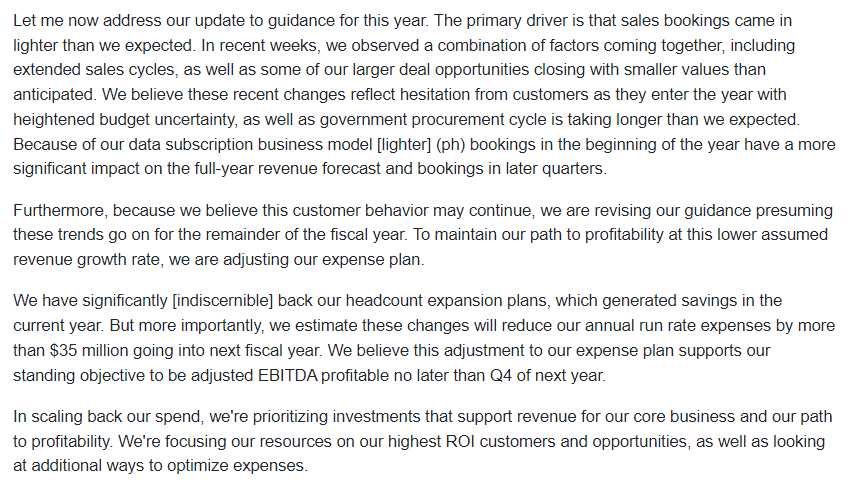

When PL came public in December 2021, the company projected a total addressable market of $128 billion. Now, less than two years later, PL seems to be hitting a sales wall at a mere $230-$250 million level. That’s like a quarter of a percent of the TAM. Something is not adding up. This is what PL said during the Q1 call in June 2023:

This is all plug and play buzz word excuses… “sales bookings came in lighter than expected”… “extended sales cycles” … “hesitation from customers” … “budget uncertainty” … blah, blah, blah. And as one would expect…

So now, less than two years after coming public, PL is running against the wind?

Conclusion:

The Q1 earnings report was a red flag, no doubt about that, and it is unclear to me how PL will get things back on track. The economy is actually pretty strong, and if PL is struggling with customer bookings at this time, then one has to wonder what happens when the economy really starts to struggle. To me, the main problem with PL is that they don’t have a viable sales strategy, they don’t seem to understand their market or customer needs, and they seem to have a weirdly opaque pricing structure making it very difficult to understand where the sales leverage comes from. In sum, PL is a science project searching for a sales strategy and sustainable business plan.

All that being said, there is some value with PL and I could see the AI angle really take off for the company. I honestly think that’s the only thing they have going for it at the moment. My guess is probably 90% of their enterprise value is based on AI hype. But, again, it is unclear how PL will monetize any of that. In truth, PL is probably be better suited being an add on to existing software package. But the public benefit nature of their corporate structure makes that less likely.

I am long PL.

References:

Planet (PL) V (April 1, 2023)

Planet Earnings (September 17, 2022)

Planet Labs (June 15, 2022)

Planet Labs II (April 16, 2022)

Planet Labs (December 21, 2021)