Planet Labs (PL) reported earnings after the market close on June 14th, and held a call later that night. In addition, PL announced an expanded strategic relationship with Bayer. Though, I did not see any financial terms or a discussion of specific resources being committed to the effort, so I am not sure how significant this announcement is. This is what I wrote about PL back in April:

To date, PL seems to be executing pretty well. The company has hit revenue targets for 2022 and projects 2023 revenues at $170-$190 million for 2023. This is below their September 2021 Analyst day projections for 2023 of $191 million in sales. But the company could be playing the earnings expectations game so I would not read too much into the 2023 sales forecasts. I like PL, and I do own stock in the company.

But at this valuation there does not seem to be any margin of safety. I wonder how big the satellite imagery market really is. I have no doubt there is a growing niche of sectors that would benefit from PL’s data, but is it really as big as PL and other companies claim it is? I am not sure. The bull case for PL is that there is large, unmet need for satellite data and ancillary information like water levels or temperatures their stacks might be able to provide. The bear case is that the market is really not that big and companies would not pay for a standalone satellite imagery service or even as part of a stack/API. Meanwhile, satellite imagery is competitive and, at least for now, pretty capital intensive. And I also wonder about how PL’s data or mapping is really any better than a competitors’. A map is a map, no? Is speed such a big deal? Time will tell.

[DISCLAIMER: I am not an expert on this company or sector. So do not rely on this information or analysis as a basis for investment. This is a highly speculative piece that is for information purposes only. At the time of this writing, I do have a position in PL. But that could change at a later date.]

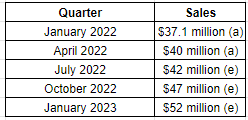

For the quarter ending April 30, 2022, PL reported sales of about $40 million, and projected sequential quarter revenues to be at between $41-$43 million. Full year FY 2023 sales are projected at between $177-$187 million. In March, PL guided FY 2023 revenues (for the period ending January 2023) at between $170-$190 million. So at the high end, the guidance was lowered a little. All things considered, this is not a big deal. Using these numbers, you can sort of guesstimate projected revenues. I put together this table of quarterly revenues1:

If you consider inflation, sales for the last two quarters and the next are basically flat.

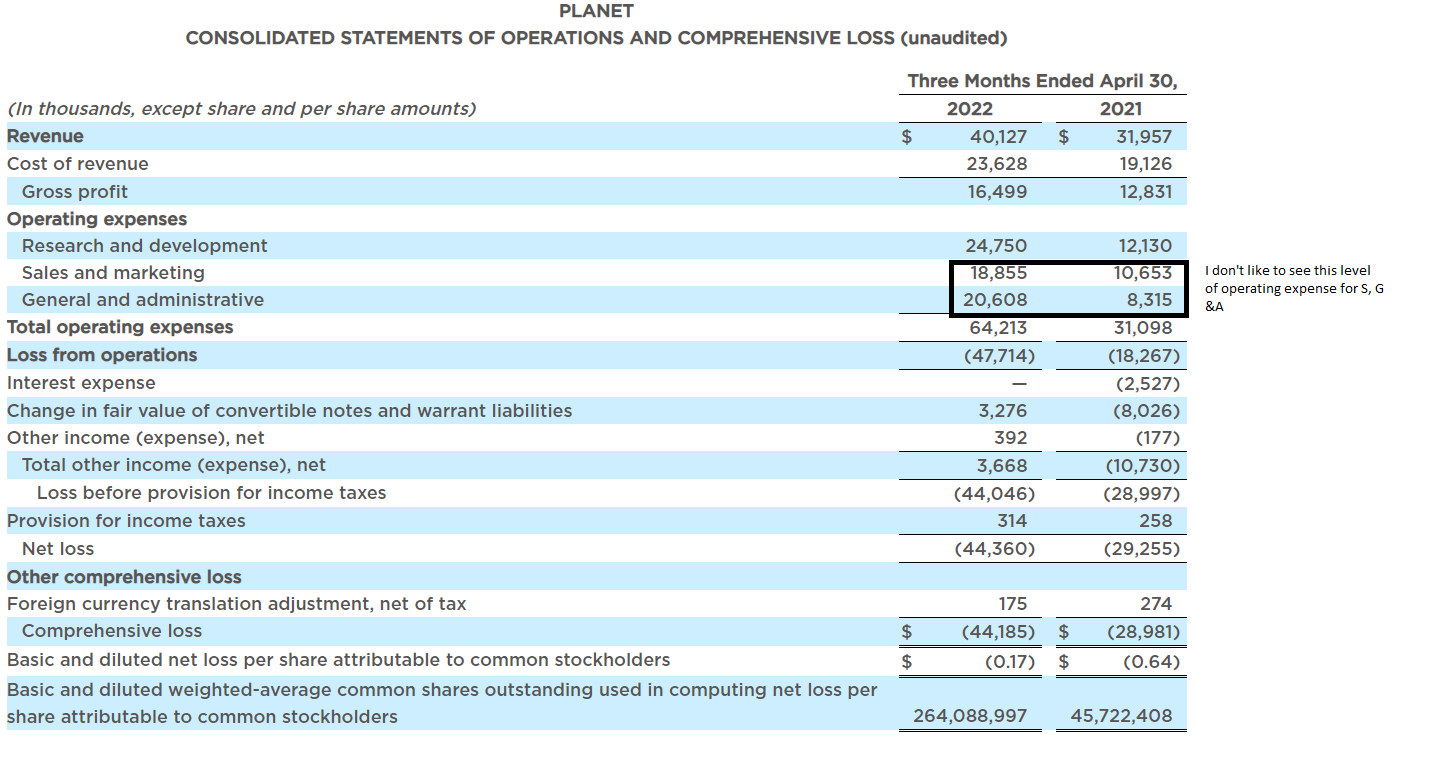

This is the income statement:

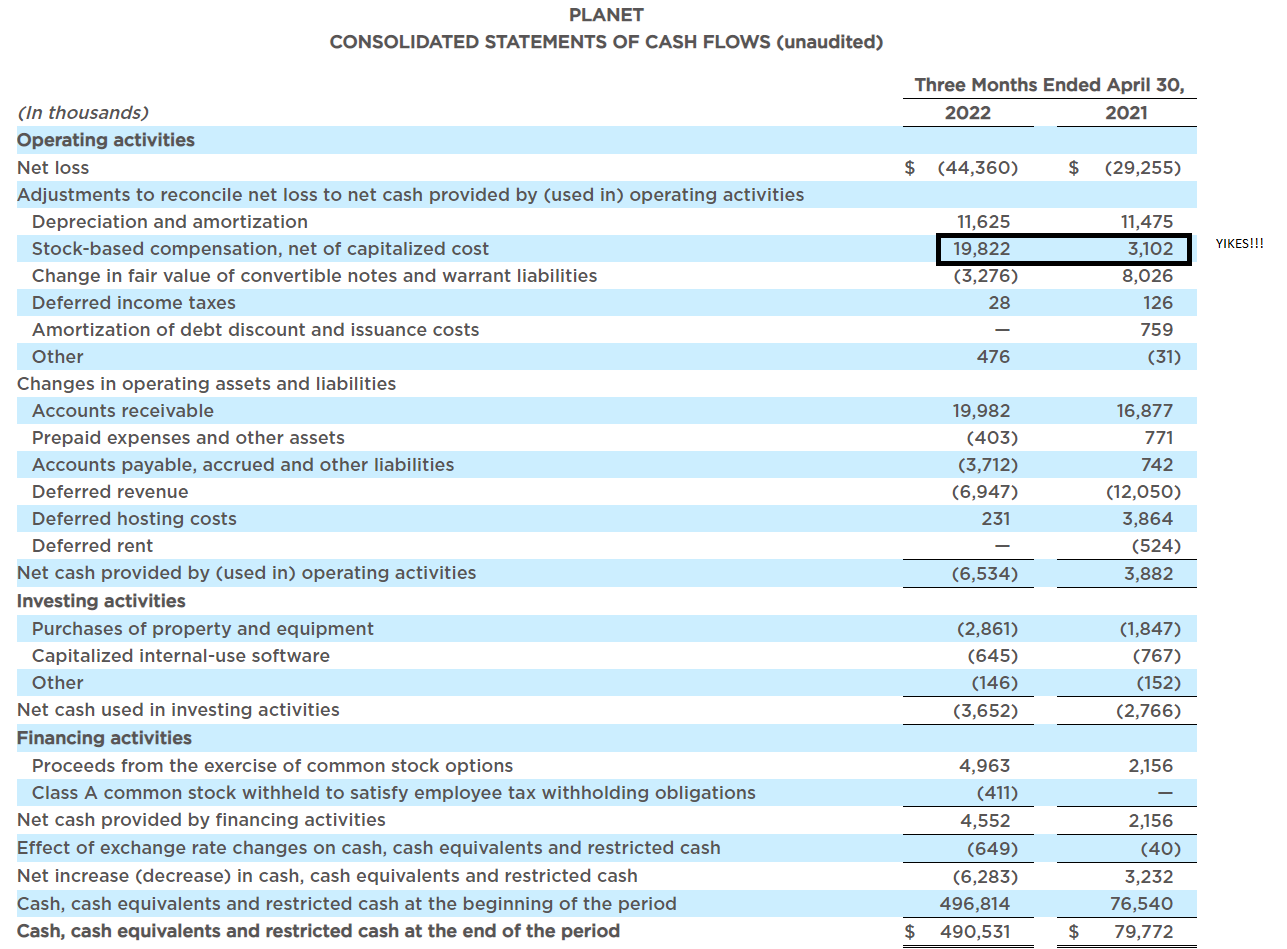

My concern here is what I noted from the prior quarter that the company is hemorrhaging cash to increase sales. There just is no signal here of any operating leverage. And then there is this:

The companies use of stock based compensation and reporting non-GAAP numbers is a problem. Stock based compensation is real and it represents about 50% of sales. This will act as a slow burn on the share price…

Killer App

In researching PL, I keep wondering what the killer app is. What is going to draw people to use their service? Will Marshall does a good job of sort of hinting at what is possible:

We basically sell imagery on a per-unit area basis: kilometers, hectares, mainly just area. The more area you get, there is a volumetric discount, but obviously pay more. We do have a lot of pricing power, I agree. Right now there's no one else that does this. To your point, it's very hard to get this data set. You have to erect a huge satellite fleet and ground stations, mission control systems, data processing and all the rest. So it's certainly not for the faint of heart, so it would take many years for somebody to build such a system. And of course, we're not going to sit on our hands, we're going to constantly improve it. That data archive, it's impossible to go back and get. It's actually, there's some really important moats around what we've built, but yes, we do have a fair bit of pricing power, some level it's value based pricing.

But I do think that what's most important for us is where we going next is not just the imagery and selling the imagery, but selling information products derived from that imagery, what we call "going up the stack." The main thing we are doing today and the reason we're going public, one of them is, of course, we have capital to then deploy. The main areas we're deploying in, one is the sales and marketing to go off the vertical market we already know work like agriculture, civil government and the ones I was describing. The second thing is that there's loads of potential to other markets, but they need more than images. Hedge funds could get huge value out of our data. I mean, we know how well crops are doing before anyone else, the whole world saw your yield. We know the output from all the world's copper mines before anyone else.

So presumably, those things are really valuable to those commodity prices. However, they do not want those pictures. They want a time-series-calibrated date. We have the data to underpin that, but we haven't built the analytics that enable us that yet. So the other side of what we are doing is investing in what we call going up the stack, and then we'll be charging more and more for just information products derived from the data. Anyway, a little bit of a long-winded answer to your question, but mainly it's volumetric based on the amount of data, but also as we go up, the value stack will be charging more for those, if you like, smaller bits of data that we can drive from the imaging.

This is more of the promise:

Yeah, with time, we will increase that as well. So it's not just pretty pictures, actually. You can't even see these things. We do do forced color images of them. But for example, that near infrared band, as I said, we can tell it's wheat and it's doing this well. And that is how it gets into this agricultural application, which is actually our biggest market. We can tell crop type and yield in every farmer's field, in every bit of the farmer field, that three by three meter box, we can say, how well is the crop doing? Does it need fertilizer? Does it need harvesting? When does it need water? And so actually, yes, we're already getting other information.

And then that's before we build analytics on top of that, that other things that automatically detect certain things like we automatically with machine learning, pull out roads, buildings, ships, planes. So you can now, if you're interested in shipping, you could circle the top 10 ports of the world, just tell me how many ships there are in these ports over time. That's all I want. I don't want to look at the pictures at all. You can now do that on our platform. Now, you can't do everything. You might ask some other questions we don't yet answer, but we're trying to get better and better so that one can actually not have to have a PhD in geospatial science to understand this imagery, but rather actually everyone could get information and value out of the imagery every day.

This all sounds great, right? Like PL is going to completely change the world. But the picture is a bit more complicated. I think the Up Ag Insights Substack did a great job of parsing out some of the challenges with PL and the agriculture vertical:

Imagery becomes more valuable to farmers and agronomists when used in combination with other layers of information. And becomes less valuable when used as a singular data layer, at least from an agronomic use case.

One key for organizations like Planet to not only maintain their revenue levels, but grow them and create more stickiness for agribusinesses will be R&D that leverages the combining of imagery to ground truthed data to create models and using those images and models in conjunction with many other layers. Remotely sensed information is only one aspect to inform models and decisions. Ground data is instrumental.

It can be argued satellite companies should focus on the imagery acquisition and create strong partnerships with the on the ground organizations, like Ag specific companies, aggregating data to be able to unlock more value from the satellite imagery.

I think this is spot on. It is an incredible insight. And it gets at the heart of the issue for PL. This is a data company. It’s sitting on a massive amount of data, it’s producing a massive amount of data. In theory, this data has a ton of killer applications. But is that really true? To me, that’s the issue. I mean, if you believe Will Marshall’s statements above about how PL’s data can help farmers economize their usage of fertilizer, why aren’t they printing money? Fertilizer prices are skyrocketing. If PL’s data can improve usage, why isn’t the company touting that? Their ag sales should be going up a lot more. Instead, they are announcing “strategic partnerships”.

Conclusion

I think PL is an interesting company and I do have a position. But, I reduced it a bit and I will stay patient with this one. The primary concern I have with PL is the macro environment is highly unfavorable for them, and my best guess is that it will take PL a couple years to build out the functionality and scale to make this into a sustainable business that can generate free cash flow. There are a lot of positives to the story, but the valuation is not favorable in this environment. That’s my opinion.

I am long PL.

For the October and January 2023 quarter numbers, I assumed about a 12% sequential growth in revenues from prior quarters. This gets to the midpoint of the full year FY 2023 range ($182 million).